The Freight 50: 2018’s top carriers standing strong in the face of headwinds

Moving on up (or down)

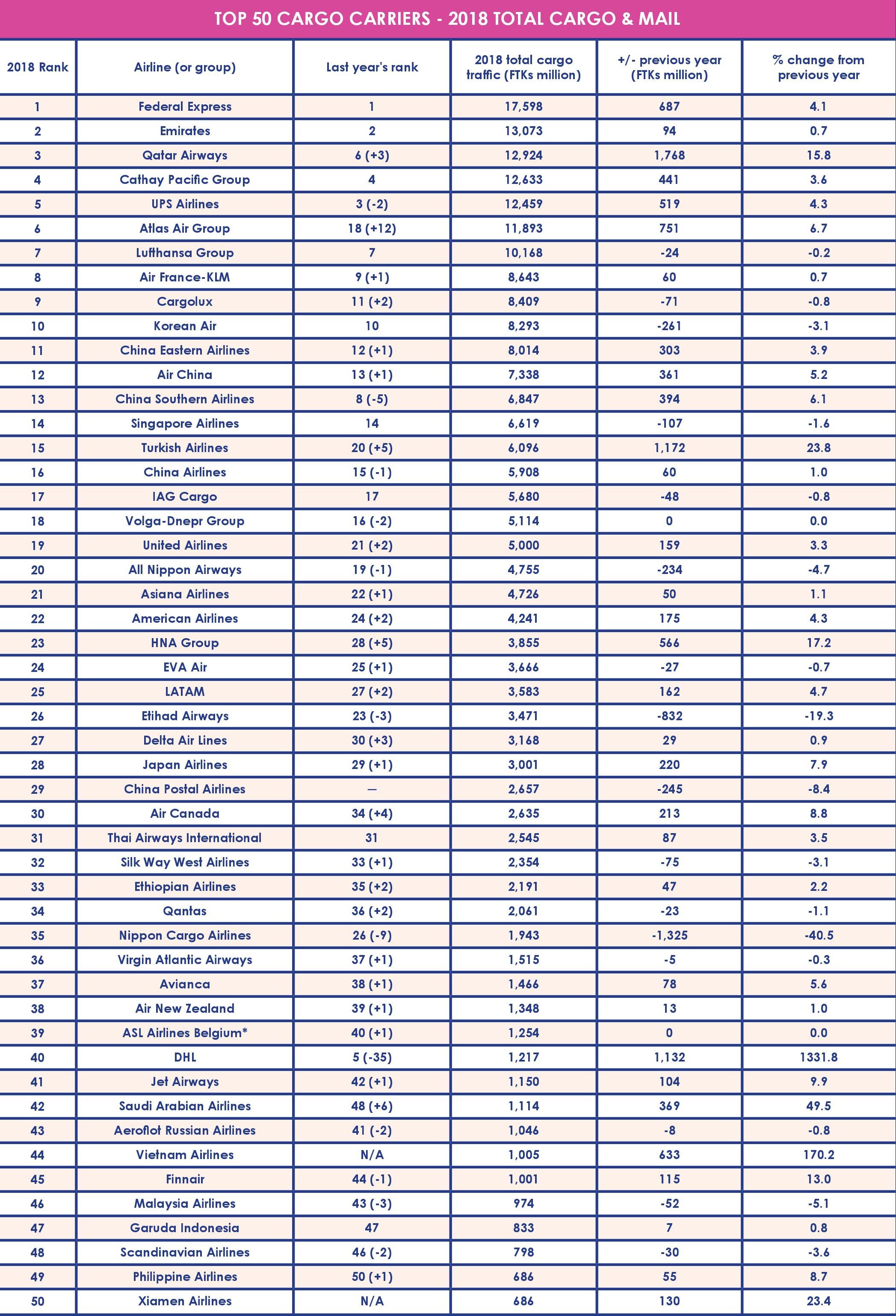

Coming in at No. 6 this year is Atlas Air Group, which reported 6.7% traffic growth on increased flying for large customers like Amazon, Asiana, and Nippon Cargo Airlines. This year, Atlas climbed 12 spots to its new 2018 ranking thanks to changes in classification methodology. In previous years, because much of the cargo moved on Atlas metal was transported for DHL Express, traffic flown by Atlas carriers was attributed to DHL Express totals. This year the Atlas Air Group includes traffic reported by Atlas Air, Polar Air Cargo and Southern Air, which all share the same operational platform and belong to parent Atlas Air Worldwide Holdings.

Traffic attributed to DHL meanwhile, now includes only traffic moving on DHL metal. The majority of DHL’s airfreight moves via other carriers operating on that integrator’s behalf, with DHL itself owning only a fraction of the aircraft providing lift on its behalf. Last year saw that change somewhat, thanks to an order DHL placed with Boeing for 14 777 freighters. DHL still appears on the 2018 Freight 50 list, at No. 40, with y-o-y traffic of 1.22 billion FTKs – more than ten times that reported for 2017.

Facing the pressure

To mitigate the impacts of a more challenging outlook for airfreight, carriers are working to more efficiently leverage their fleets and cater to more specialized customer demand.

LATAM Cargo, which for 2018 climbed two spots to break into the top 25, told Air Cargo World that while most of the world’s focus has been on trade tensions between the U.S. and China, Latin American carriers have faced their own obstacles with “economic and political instability in Argentina and Brazil.”

“During 2018 we addressed this by maintaining a robust, customer-focused freighter itinerary, leveraging our international belly capacity and driving efficiency initiatives,” with LATAM’s approach “centered on completing the standardization of our freighter fleet around our Boeing 767-300Fs, redesigning our freighter schedules by adding new ODs, improving connectivity on our main passenger hubs and improving employee productivity,” the carrier added.

Luxembourg-based Cargolux, which moved into the top 10 carriers with 2018 traffic of 8.41 billion FTKs, told Air Cargo World that “increased demand for Cargolux’s specialized products significantly contributed to the bottom-line.” In addition to specialty shipment offerings including CV alive, CV power and CV jumbo – for live animals, engine-powered items and outsized cargo, respectively – Cargolux saw strong charter demand during 2018, the carrier said, “driven by the Europe-North America trade lane, in particular.”

With airfreight’s peak season still to come, anxieties about how much airfreight demand will materialize have been top-of-mind. Regarding outlooks for the rest of 2019, “we do not expect the market to drastically change but we still expect a peak season,” Qatar’s Halleux added. “The levels of charter pre-bookings for this winter are encouraging.”

Regarding the ongoing trade conflict between the U.S. and China, a Korean Air spokesperson said, “Although the U.S.-China trade dispute is normally regarded as bad news, we still need to keep an eye on the situation of Southeast Asian routes, since there are global companies considering the shift of their production base in China to Southeast Asia.”

“We are rapidly responding to market changes by increasing capacity to Southeast Asia in preparation for stagnation in the Chinese market,” Korean Air added.